Islamic finance presents $6tn opportunity

Increased digitalisation and emergence of Islamic products aligned with sustainability themes are opening up new avenues for growth

The global Islamic finance industry is expected to grow to $5.9tn by 2026 up from $4tn in 2021, according to an Islamic Finance Development (IFDI) 2021 report. By IFDI projections, this growth will be driven by the sector’s biggest segments – Islamic banks and sukuks.

This sector has continued its growth momentum despite the challenges of a recovering economy, which has been affected in large part by energy prices, disruption in supply chain and rising inflation.

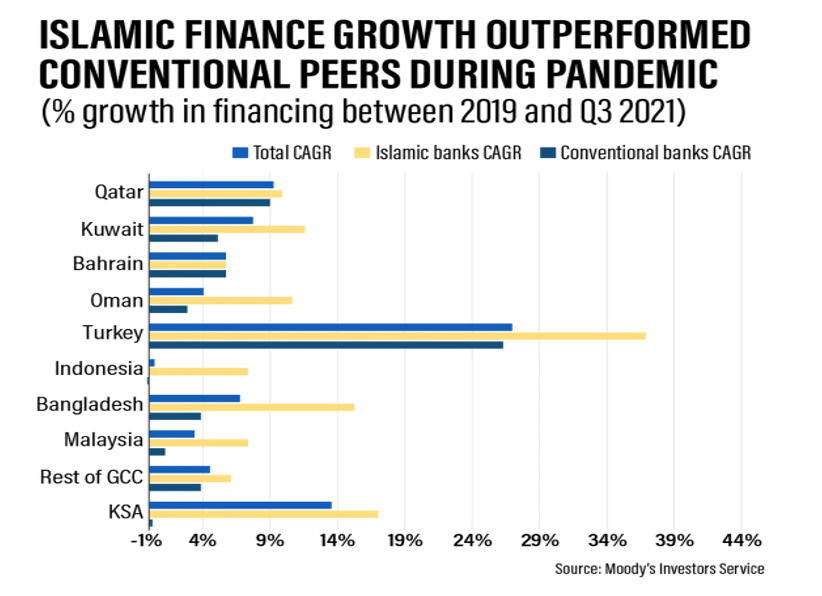

In fact, Islamic financing has expanded at a much faster rate in the past few years compared with conventional loan growth. Moody’s Investors Service states that the two segments grew at an average compound rate of 10.5 per cent and 3.4 per cent respectively during the 2020-21 period.

The outlook for the Islamic financial system is optimistic as experts now regard it as one of the fastest growing segments of the global financial system, with a predicted average growth rate of 8 per cent until 2025.

New developments

Although the market is still at a maturingstage, considerable growth opportunities are emerging, particularly with the increased focus on aligning Islamic financial products with environmental, social and governance (ESG) factors and the recent strides in digitalisation.

“Green and sustainability sukuk are providing the additional impetus to the overall demand for the Islamic papers by the global investors as they are aligned with sustainability themes. The implementation of energy transition strategies and investments in clean energy are also boosting the opportunities for sustainable sukuk.

The Islamic banking sector holds the lion’s share of the market, constituting 70 per cent of Islamic finance assets, as per Refinitiv Islamic finance data. Sukuk is the second-largest contributor to Islamic finance assets with over $74.5bn of issuances in the first half of 2022 according to S&P Global Ratings.

“Islamic finance has played a vital role in the UAE’s national development with Islamic banking and finance assets estimated to be about 25 per cent of the total domestic banking assets, which stood at AED1.6tn in August 2022,” said Sohail Zubairi, AAOIFI certified sharia advisor and auditor and IICRA accredited Islamic finance arbitration expert, speaking during the MEED-Mashreq Islamic Business Leaders Forum on 7 December 2022.

“We need a Sukuk insurer entity in the UAE on the lines of Danajamin in Malaysia that can help wean the private entities away from the banking sector and into the domestic capital market. This move will help reduce the burden on the UAE banks that can then spare greater funding at lower costs for the projects of national development,” said Zubairi.

To capitalise on the rising demand and to keep pace with the developments in this segment, the industry must produce an emerging pool of talent that can integrate the knowledge of sharia and Islamic products with the technological advances in the industry.

However, existing training and qualifications may not provide the required levels of specialisation and sophistication.

“In many countries, especially ones with low awareness, Islamic finance practitioners are often inadequately equipped,” said Bashar al-Natoor, global head of Islamic finance at Fitch Ratings. “There is a gap in understanding sharia products and the industry is looking to employ specialists.

“Stakeholders, including customers, regulators and employees of Islamic financial institutions often view Islamic products to be similar to conventional interest-based products. This perception stems from the way Islamic products are marketed and priced.”

A major contributor to this sector’s continued growth will be making sharia-compliant products easily accessible and standardising compliance processes.

Furthermore, as digital banks and new payment methods such as ‘buy now, pay later’ emerge in the Islamic finance system, it is important that Islamic banks not only simplify and centralise their operating models but also work with the innovators and developers to deliver banking solutions without compromising sharia principles.

Citing collaboration as another key driver for the growth of Islamic finance, senior corporate and structured finance and banking leader and Islamic finance specialist Jawaad Chawla said, “From a very humble beginning, not more than 2 decades ago, Islamic finance has grown into a multi-trillion-dollar industry. And we got here through the collaborative efforts of bankers, lawyers, scholars, regulators and industry experts, who have all come together to bring innovation into Islamic finance and offer it to a wider audience.”

Globalisation trend

Islamic finance is no longer exclusive to Islamic or Muslim-majority countries. Recent global developments such as the UK government’s second issuance of sukuk in 2021 and the launch of Australia’s first full-fledged Islamic bank in July 2022 are a testament to its increasing appeal.

Zubairi explained that more and more countries are now keen to adopt Islamic finance options as governments move to diversify funding options and interest in sustainable and responsible investing peaks.

“We are seeing countries such as Hong Kong and South Africa adopting Islamic finance and a rise in investments from countries that do not necessarily have a Muslim dominated population,”he said. He further opined that the growth in Islamic finance assets is reaching saturation point in the Islamic world and that next generation push can only come from non-OIC countries provided “we are able to develop a global Islamic finance law which provides legal protection to the parties entering into an Islamic finance contract and also serves as a global benchmark for dispute resolution”.

This globalisation trend is expected to continue with the application of ESG principles and digitalisation and a higher degree of standardisation within the Islamic finance sector.

Key characteristics of sharia-compliant or halal investing

|